library(tseries)

library(fGarch)

library(rugarch)

library(MASS)ARCH/GARCH in R

tseries package (not recommended)

The most basic GARCH fitting I know is done in the tseries package. I do not recommend it because it does not allow you to easily combine the variance model with a mean model.

data(SP500)

tseries.arma <- arma(SP500,order=c(1,1))

summary(tseries.arma)

Call:

arma(x = SP500, order = c(1, 1))

Model:

ARMA(1,1)

Residuals:

Min 1Q Median 3Q Max

-7.245862 -0.460612 -0.002503 0.498085 4.749524

Coefficient(s):

Estimate Std. Error t value Pr(>|t|)

ar1 0.911630 0.056856 16.03 <2e-16 ***

ma1 -0.932451 0.048937 -19.05 <2e-16 ***

intercept 0.004304 0.002929 1.47 0.142

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Fit:

sigma^2 estimated as 0.8951, Conditional Sum-of-Squares = 2486.73, AIC = 7587.37tseries.garch <- garch(residuals(tseries.arma)[-1],order=c(1,1))

***** ESTIMATION WITH ANALYTICAL GRADIENT *****

I INITIAL X(I) D(I)

1 8.056347e-01 1.000e+00

2 5.000000e-02 1.000e+00

3 5.000000e-02 1.000e+00

IT NF F RELDF PRELDF RELDX STPPAR D*STEP NPRELDF

0 1 1.195e+03

1 4 1.179e+03 1.32e-02 6.30e-02 1.2e-01 1.9e+03 2.0e-01 6.00e+01

2 6 1.169e+03 8.89e-03 1.22e-02 4.2e-02 3.8e+00 7.0e-02 1.93e+01

3 8 1.148e+03 1.78e-02 2.01e-02 1.6e-01 2.5e+00 2.4e-01 1.14e+01

4 9 1.094e+03 4.65e-02 6.46e-02 5.6e-01 2.0e+00 4.9e-01 1.33e+01

5 11 1.049e+03 4.13e-02 6.16e-02 3.2e-02 3.3e+00 4.9e-02 8.36e+00

6 12 1.041e+03 8.24e-03 9.32e-03 3.8e-02 2.0e+00 4.9e-02 4.10e+01

7 13 1.024e+03 1.55e-02 2.31e-02 7.1e-02 2.0e+00 9.8e-02 2.06e+01

8 14 1.004e+03 1.96e-02 2.74e-02 7.1e-02 2.0e+00 9.8e-02 4.99e+00

9 15 9.792e+02 2.51e-02 2.77e-02 5.4e-02 2.0e+00 9.8e-02 9.22e+00

10 16 9.633e+02 1.63e-02 2.66e-02 5.3e-02 2.0e+00 9.8e-02 9.72e+00

11 17 9.608e+02 2.57e-03 2.95e-02 4.9e-02 2.0e+00 9.8e-02 9.17e+00

12 19 9.436e+02 1.79e-02 6.55e-02 5.9e-03 3.6e+00 1.1e-02 2.84e+00

13 20 9.355e+02 8.60e-03 1.15e-02 5.2e-03 2.0e+00 1.1e-02 8.72e+00

14 21 9.338e+02 1.81e-03 2.36e-03 5.2e-03 2.0e+00 1.1e-02 2.46e+00

15 22 9.313e+02 2.67e-03 3.47e-03 4.4e-03 2.0e+00 1.1e-02 1.36e+00

16 25 9.240e+02 7.80e-03 9.47e-03 1.8e-02 1.9e+00 4.4e-02 7.69e-01

17 28 9.238e+02 2.53e-04 1.16e-03 5.5e-04 3.0e+00 1.2e-03 7.50e-02

18 29 9.235e+02 3.26e-04 3.28e-04 4.6e-04 2.0e+00 1.2e-03 2.41e-02

19 30 9.234e+02 1.03e-04 1.40e-04 6.1e-04 3.6e+00 1.2e-03 2.60e-02

20 31 9.232e+02 2.67e-04 3.09e-04 1.2e-03 2.0e+00 2.5e-03 2.68e-02

21 32 9.231e+02 7.26e-05 4.07e-04 1.2e-03 1.5e+01 2.5e-03 1.79e-02

22 33 9.230e+02 4.79e-05 5.36e-04 1.0e-03 2.0e+00 2.5e-03 2.20e-02

23 34 9.227e+02 3.95e-04 4.24e-04 5.6e-04 2.0e+00 1.2e-03 9.10e-03

24 36 9.223e+02 4.70e-04 5.97e-04 2.7e-03 1.8e+00 7.1e-03 7.14e-03

25 38 9.221e+02 2.18e-04 3.01e-04 1.2e-03 1.4e+00 2.5e-03 9.48e-04

26 39 9.220e+02 6.27e-05 7.74e-05 9.3e-04 9.5e-01 2.5e-03 1.47e-04

27 40 9.220e+02 2.65e-05 6.35e-05 9.9e-04 8.5e-01 2.5e-03 9.74e-05

28 41 9.220e+02 7.69e-06 8.82e-06 7.9e-05 0.0e+00 2.0e-04 8.82e-06

29 42 9.220e+02 1.05e-07 9.11e-08 2.4e-05 0.0e+00 5.6e-05 9.11e-08

30 43 9.220e+02 1.06e-09 2.99e-10 2.9e-06 0.0e+00 7.5e-06 2.99e-10

31 44 9.220e+02 -3.14e-11 4.29e-12 2.3e-07 0.0e+00 5.4e-07 4.29e-12

***** RELATIVE FUNCTION CONVERGENCE *****

FUNCTION 9.219615e+02 RELDX 2.309e-07

FUNC. EVALS 44 GRAD. EVALS 31

PRELDF 4.289e-12 NPRELDF 4.289e-12

I FINAL X(I) D(I) G(I)

1 4.444827e-03 1.000e+00 -7.100e-02

2 5.091469e-02 1.000e+00 -4.831e-02

3 9.457935e-01 1.000e+00 -4.780e-02summary(tseries.garch)

Call:

garch(x = residuals(tseries.arma)[-1], order = c(1, 1))

Model:

GARCH(1,1)

Residuals:

Min 1Q Median 3Q Max

-7.045125 -0.550290 -0.003681 0.585257 4.015891

Coefficient(s):

Estimate Std. Error t value Pr(>|t|)

a0 0.004445 0.001063 4.182 2.89e-05 ***

a1 0.050915 0.004427 11.500 < 2e-16 ***

b1 0.945793 0.004771 198.236 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Diagnostic Tests:

Jarque Bera Test

data: Residuals

X-squared = 833.78, df = 2, p-value < 2.2e-16

Box-Ljung test

data: Squared.Residuals

X-squared = 0.38262, df = 1, p-value = 0.5362# estimates of iid normal errors omega_t

(tseries.omega <- head(residuals(tseries.garch)))[1] NA -0.6894459 0.5386388 -0.9365332 -0.5005003 0.4036426# estimates of past conditional sd sigma_t

(tseries.sigma_past <- head(fitted(tseries.garch)[,1]))[1] NA 1.141019 1.125747 1.105339 1.102067 1.081042# forecasts of future conditional sd sigma_t

(tseries.sigma_future <- head(predict(tseries.garch)[,1]))[1] NA 1.141019 1.125747 1.105339 1.102067 1.081042In my opinion, this package has the most limited implementation and is strictly dominated for every use case by one of the two packages below.

fGarch package (functional but not my first choice)

ARCH/GARCH analysis in R was, in years past, primarily performed through the fGarch package, which offers model definition, prediction, plotting, etc. through familiar interfaces. The package is still maintained and offers solid support for basic and intermediate use cases.

Although not shown in the code below, the predict() method simultaneously predicts for both the mean and the variance (we are extracting only the variance).

fgarch.armagarch <- garchFit(SP500 ~ arma(1,1) + garch(1,1), data=SP500)

Series Initialization:

ARMA Model: arma

Formula Mean: ~ arma(1, 1)

GARCH Model: garch

Formula Variance: ~ garch(1, 1)

ARMA Order: 1 1

Max ARMA Order: 1

GARCH Order: 1 1

Max GARCH Order: 1

Maximum Order: 1

Conditional Dist: norm

h.start: 2

llh.start: 1

Length of Series: 2780

Recursion Init: mci

Series Scale: 0.9477464Warning in arima(.series$x, order = c(u, 0, v), include.mean = include.mean):

possible convergence problem: optim gave code = 1Parameter Initialization:

Initial Parameters: $params

Limits of Transformations: $U, $V

Which Parameters are Fixed? $includes

Parameter Matrix:

U V params includes

mu -0.48275223 0.4827522 0.04829772 TRUE

ar1 -0.99999999 1.0000000 -0.17030411 TRUE

ma1 -0.99999999 1.0000000 0.18933184 TRUE

omega 0.00000100 100.0000000 0.10000000 TRUE

alpha1 0.00000001 1.0000000 0.10000000 TRUE

gamma1 -0.99999999 1.0000000 0.10000000 FALSE

beta1 0.00000001 1.0000000 0.80000000 TRUE

delta 0.00000000 2.0000000 2.00000000 FALSE

skew 0.10000000 10.0000000 1.00000000 FALSE

shape 1.00000000 10.0000000 4.00000000 FALSE

Index List of Parameters to be Optimized:

mu ar1 ma1 omega alpha1 beta1

1 2 3 4 5 7

Persistence: 0.9

--- START OF TRACE ---

Selected Algorithm: nlminb

R coded nlminb Solver:

0: 3707.8226: 0.0482977 -0.170304 0.189332 0.100000 0.100000 0.800000

1: 3695.1512: 0.0483008 -0.169151 0.190394 0.0787674 0.103273 0.793089

2: 3683.1731: 0.0483048 -0.167750 0.191673 0.0771166 0.122061 0.805435

3: 3670.4420: 0.0483162 -0.164180 0.194885 0.0364971 0.141012 0.809289

4: 3660.5110: 0.0483495 -0.155768 0.202148 0.0273841 0.154717 0.849936

5: 3654.5379: 0.0484140 -0.147342 0.207997 0.00549702 0.128500 0.877750

6: 3642.7519: 0.0485273 -0.135221 0.215353 0.0234248 0.0902875 0.885425

7: 3633.9451: 0.0485836 -0.156626 0.189896 0.0136500 0.0797515 0.912497

8: 3633.0063: 0.0485839 -0.156566 0.189943 0.0105706 0.0785118 0.911182

9: 3631.5382: 0.0485888 -0.156336 0.189948 0.0110774 0.0774069 0.914531

10: 3628.8437: 0.0486198 -0.155502 0.189330 0.00610671 0.0651190 0.931398

11: 3628.8374: 0.0486200 -0.155467 0.189358 0.00690257 0.0652188 0.931793

12: 3628.6730: 0.0486201 -0.155451 0.189370 0.00658121 0.0649747 0.931600

13: 3628.5997: 0.0486210 -0.155299 0.189488 0.00669202 0.0641082 0.931629

14: 3628.4960: 0.0486285 -0.155665 0.188738 0.00693647 0.0631391 0.932849

15: 3628.3416: 0.0486403 -0.155732 0.188093 0.00658872 0.0618761 0.933853

16: 3627.7023: 0.0487967 -0.146041 0.190608 0.00583606 0.0549905 0.941102

17: 3627.6803: 0.0487968 -0.146045 0.190601 0.00569596 0.0549451 0.941058

18: 3627.6708: 0.0487975 -0.146078 0.190535 0.00557499 0.0550521 0.941321

19: 3627.6631: 0.0488039 -0.146242 0.190071 0.00541304 0.0547618 0.941502

20: 3627.6405: 0.0488109 -0.146398 0.189590 0.00547456 0.0545710 0.941794

21: 3627.6121: 0.0488414 -0.146682 0.187899 0.00534687 0.0538378 0.942507

22: 3627.6109: 0.0488415 -0.146681 0.187896 0.00538884 0.0538604 0.942550

23: 3627.6098: 0.0488430 -0.146647 0.187864 0.00536123 0.0538500 0.942546

24: 3627.6089: 0.0488460 -0.146581 0.187797 0.00535714 0.0538544 0.942608

25: 3627.6071: 0.0488527 -0.146427 0.187652 0.00533035 0.0538425 0.942600

26: 3627.0126: 0.0582226 0.0691733 -0.0144367 0.00556139 0.0577318 0.939071

27: 3626.9127: 0.0590365 0.0879504 -0.0393038 0.00579615 0.0551005 0.940415

28: 3626.8679: 0.0577092 0.100899 -0.0568744 0.00483480 0.0520673 0.945062

29: 3626.8128: 0.0559977 0.102990 -0.0584852 0.00482603 0.0520600 0.944805

30: 3626.7555: 0.0542885 0.105033 -0.0606813 0.00516634 0.0527725 0.943858

31: 3626.7335: 0.0545761 0.0799272 -0.0362296 0.00520082 0.0531745 0.943421

32: 3626.7274: 0.0513309 0.0971461 -0.0517508 0.00521763 0.0532398 0.943295

33: 3626.7245: 0.0527050 0.0870950 -0.0425974 0.00535179 0.0536743 0.942666

34: 3626.7237: 0.0529863 0.0806323 -0.0359524 0.00527602 0.0533714 0.943089

35: 3626.7234: 0.0525806 0.0860125 -0.0414312 0.00528154 0.0534703 0.942988

36: 3626.7234: 0.0526617 0.0850928 -0.0404383 0.00529002 0.0534592 0.942980

37: 3626.7234: 0.0526679 0.0850071 -0.0403745 0.00528744 0.0534593 0.942986

38: 3626.7234: 0.0526638 0.0850516 -0.0404173 0.00528753 0.0534593 0.942986

Final Estimate of the Negative LLH:

LLH: 3477.526 norm LLH: 1.250908

mu ar1 ma1 omega alpha1 beta1

0.049911944 0.085051577 -0.040417326 0.004749381 0.053459335 0.942985580

R-optimhess Difference Approximated Hessian Matrix:

mu ar1 ma1 omega alpha1

mu -5487.50292 -270.4325 27.02373 792.2338 226.0816

ar1 -270.43248 -2546.3381 -2516.58109 -1623.7710 -426.8226

ma1 27.02373 -2516.5811 -2520.78590 -1624.0013 -415.2228

omega 792.23377 -1623.7710 -1624.00131 -1800871.1748 -629448.6023

alpha1 226.08164 -426.8226 -415.22283 -629448.6023 -357310.5359

beta1 -296.61877 -1036.8765 -969.35042 -803221.5863 -402755.4115

beta1

mu -296.6188

ar1 -1036.8765

ma1 -969.3504

omega -803221.5863

alpha1 -402755.4115

beta1 -480647.1975

attr(,"time")

Time difference of 0.01929498 secs

--- END OF TRACE ---

Time to Estimate Parameters:

Time difference of 0.1493778 secssummary(fgarch.armagarch)

Title:

GARCH Modelling

Call:

garchFit(formula = SP500 ~ arma(1, 1) + garch(1, 1), data = SP500)

Mean and Variance Equation:

data ~ arma(1, 1) + garch(1, 1)

<environment: 0x143254ca8>

[data = SP500]

Conditional Distribution:

norm

Coefficient(s):

mu ar1 ma1 omega alpha1 beta1

0.0499119 0.0850516 -0.0404173 0.0047494 0.0534593 0.9429856

Std. Errors:

based on Hessian

Error Analysis:

Estimate Std. Error t value Pr(>|t|)

mu 0.049912 0.018630 2.679 0.00738 **

ar1 0.085052 0.237099 0.359 0.71981

ma1 -0.040417 0.237614 -0.170 0.86493

omega 0.004749 0.001664 2.853 0.00433 **

alpha1 0.053459 0.008028 6.659 2.75e-11 ***

beta1 0.942986 0.008508 110.839 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Log Likelihood:

-3477.526 normalized: -1.250908

Description:

Thu Mar 12 22:57:53 2026 by user:

Standardised Residuals Tests:

Statistic p-Value

Jarque-Bera Test R Chi^2 743.5736024 0.00000000

Shapiro-Wilk Test R W 0.9797477 0.00000000

Ljung-Box Test R Q(10) 17.1068851 0.07203209

Ljung-Box Test R Q(15) 28.6103664 0.01804608

Ljung-Box Test R Q(20) 32.3070958 0.04013397

Ljung-Box Test R^2 Q(10) 5.6342460 0.84499961

Ljung-Box Test R^2 Q(15) 9.3117155 0.86066293

Ljung-Box Test R^2 Q(20) 12.1598580 0.91046386

LM Arch Test R TR^2 8.7157933 0.72699462

Information Criterion Statistics:

AIC BIC SIC HQIC

2.506134 2.518933 2.506124 2.510755 # estimates of iid normal errors omega_t

(fgarch.omega <- head(residuals(fgarch.armagarch,standardize=TRUE)))[1] 0.0000000 -0.9665403 -1.0755090 0.4782480 -1.3808938 -0.7108837# estimates of past conditional sd sigma_t

(fgarch.sigma_past <- head(fgarch.armagarch@sigma.t))[1] 0.9487024 0.9238347 0.9231379 0.9279241 0.9095212 0.9322778# forecasts of future conditional sd sigma_t

(fgarch.sigma_future <- head(predict(fgarch.armagarch)[,3]))[1] 1.585127 1.583807 1.582490 1.581178 1.579868 1.578563fGARCH also allows the user to create fixed specifications which can be used for simulation purposes, and it has a nice array of diagnostic plotting tools with some user interactivity. The plots below come from a menu of 16 total diagnostics which the user can shuffle back and forth:

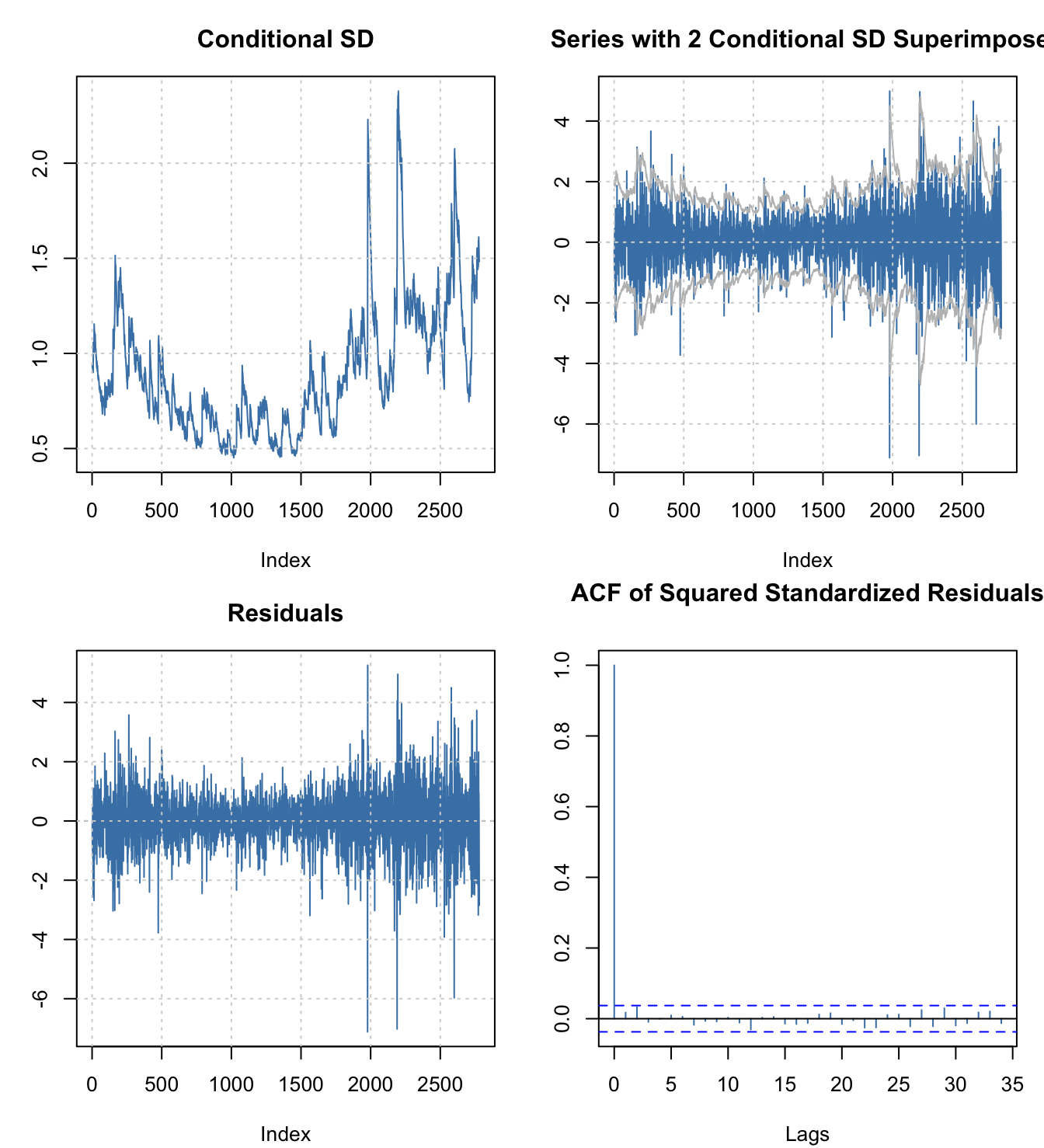

par(mfrow=c(2,2),mar=c(4,3,3,1)+0.1)

plot(fgarch.armagarch,which=c(2,3,7,11))

Ultimately, for student work, fGarch is more than enough “horsepower” for most jobs. I was tempted to use it for the two previous pages on ARCH and GARCH models. However, it has lost some industry support in favor of a newer package with more functionality and control.

rugarch package (reluctantly recommended)

rugarch (R univariate GARCH, as opposed to the companion package rmgarch for R multivariate GARCH) is more actively developed, has added more functionality, allows the user more control over the fitting details and estimation routines, contains more diagnostic tests, and has become more standard in industry use, partly because of various helper funcitons that directly solve common quesitons such as value-at-risk (VaR).

It would be very easy to recommend rugarch except that the interface is less intuitive and “user-friendly” than the earlier packages. However, on balance it would be my pick if you had to familiarize yourself with a package you intended to use professionally.

Users should specify a mean model (if any) and a variance model separately. Simulation, forecasting, and bootstrapping methods can all be used either with models fit to data or with predefined model specifications.

Although not used in the example below, external regressors can be added to both the mean and the variance equations, which is perhaps the most important upgrade over the fGarch functionality. This would allow you, for example, to add Fourier harmonics to adjust the seasonality of a mean model, or to perform a Fama-French or CAPM-style stock price analysis which controls for market behavior.

rug.spec <- ugarchspec(variance.model=list(model='sGARCH',

garchOrder=c(1,1)),

mean.model=list(armaOrder=c(1,1)))

(rugarch.armagarch <- ugarchfit(spec=rug.spec,data=SP500))

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : sGARCH(1,1)

Mean Model : ARFIMA(1,0,1)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.054483 0.014786 3.68483 0.000229

ar1 0.069644 0.236881 0.29400 0.768756

ma1 -0.024941 0.236607 -0.10541 0.916049

omega 0.004749 0.001764 2.69217 0.007099

alpha1 0.053445 0.008475 6.30652 0.000000

beta1 0.942996 0.009100 103.62261 0.000000

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.054483 0.013700 3.97684 0.000070

ar1 0.069644 0.126453 0.55075 0.581807

ma1 -0.024941 0.129047 -0.19327 0.846746

omega 0.004749 0.002715 1.74916 0.080264

alpha1 0.053445 0.015444 3.46056 0.000539

beta1 0.942996 0.016363 57.62910 0.000000

LogLikelihood : -3477.58

Information Criteria

------------------------------------

Akaike 2.5062

Bayes 2.5190

Shibata 2.5062

Hannan-Quinn 2.5108

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.1453 7.030e-01

Lag[2*(p+q)+(p+q)-1][5] 6.1896 3.578e-05

Lag[4*(p+q)+(p+q)-1][9] 9.9892 9.319e-03

d.o.f=2

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 0.8522 0.3559

Lag[2*(p+q)+(p+q)-1][5] 3.4549 0.3302

Lag[4*(p+q)+(p+q)-1][9] 4.2235 0.5514

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.2352 0.500 2.000 0.6277

ARCH Lag[5] 0.3788 1.440 1.667 0.9186

ARCH Lag[7] 0.8226 2.315 1.543 0.9406

Nyblom stability test

------------------------------------

Joint Statistic: 1.1067

Individual Statistics:

mu 0.20619

ar1 0.07068

ma1 0.07197

omega 0.16096

alpha1 0.36750

beta1 0.22933

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.49 1.68 2.12

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 1.069 0.2851017

Negative Sign Bias 1.580 0.1143060

Positive Sign Bias 1.625 0.1041982

Joint Effect 19.905 0.0001776 ***

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 63.94 9.060e-07

2 30 70.22 2.833e-05

3 40 96.43 9.084e-07

4 50 114.50 3.680e-07

Elapsed time : 0.06450582 # estimates of iid normal errors omega_t

(rugarch.omega <- head(residuals(rugarch.armagarch,standardize=TRUE)))Warning: object timezone ('UTC') is different from system timezone ('')

NOTE: set 'options(xts_check_TZ = FALSE)' to disable this warning

This note is displayed once per session [,1]

1970-01-02 -0.3306029

1970-01-03 -0.9779862

1970-01-04 -1.0731489

1970-01-05 0.4764113

1970-01-06 -1.3781128

1970-01-07 -0.7088005# estimates of past conditional sd sigma_t

(rugarch.sigma_past <- head(sigma(rugarch.armagarch)))Warning: object timezone ('UTC') is different from system timezone ('') [,1]

1970-01-02 0.9478858

1970-01-03 0.9258873

1970-01-04 0.9257269

1970-01-05 0.9303843

1970-01-06 0.9118774

1970-01-07 0.9344897# forecasts of future conditional sd sigma_t

(rugarch.sigma_future <- head(sigma(ugarchforecast(rugarch.armagarch)))) 1977-08-12

T+1 1.584798

T+2 1.583476

T+3 1.582158

T+4 1.580843

T+5 1.579531

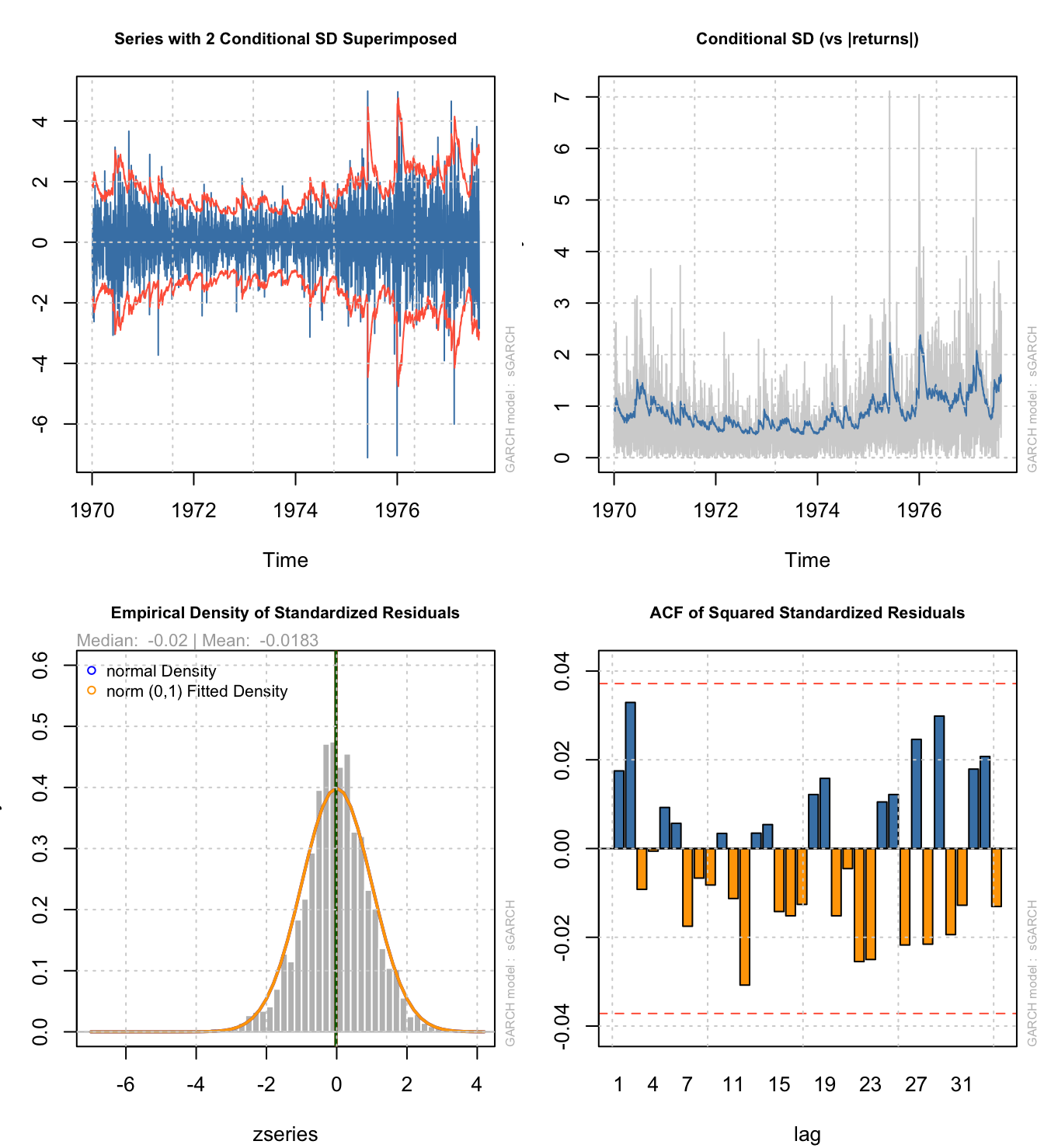

T+6 1.578224The rugarch package also contains most of the same plotting tools as fGarch:

par(mfrow=c(2,2),mar=c(4,3,3,1)+0.1)

plot(rugarch.armagarch,which=c(1))

plot(rugarch.armagarch,which=c(3))

plot(rugarch.armagarch,which=c(8))

plot(rugarch.armagarch,which=c(11))

In the end, your results should not vary wildly between fGarch and rugarch, though the more limited functionality of tseries may well affect your results:

# Standardized residuals:

cbind(tseries=tseries.omega,

fGarch=fgarch.omega,

rugarch=rugarch.omega)Warning: object timezone ('UTC') is different from system timezone ('') tseries fGarch rugarch

1970-01-02 NA 0.0000000 -0.3306029

1970-01-03 -0.6894459 -0.9665403 -0.9779862

1970-01-04 0.5386388 -1.0755090 -1.0731489

1970-01-05 -0.9365332 0.4782480 0.4764113

1970-01-06 -0.5005003 -1.3808938 -1.3781128

1970-01-07 0.4036426 -0.7108837 -0.7088005# In-sample conditional volatility:

cbind(tseries=tseries.sigma_past,

fGarch=fgarch.sigma_past,

rugarch=rugarch.sigma_past)Warning: object timezone ('UTC') is different from system timezone ('') tseries fGarch rugarch

1970-01-02 NA 0.9487024 0.9478858

1970-01-03 1.141019 0.9238347 0.9258873

1970-01-04 1.125747 0.9231379 0.9257269

1970-01-05 1.105339 0.9279241 0.9303843

1970-01-06 1.102067 0.9095212 0.9118774

1970-01-07 1.081042 0.9322778 0.9344897# Forecasted conditional volatility:

cbind(tseries=tseries.sigma_future,

fGarch=fgarch.sigma_future,

rugarch=c(rugarch.sigma_future)) tseries fGarch rugarch

[1,] NA 1.585127 1.584798

[2,] 1.141019 1.583807 1.583476

[3,] 1.125747 1.582490 1.582158

[4,] 1.105339 1.581178 1.580843

[5,] 1.102067 1.579868 1.579531

[6,] 1.081042 1.578563 1.578224